.webp)

In This Guide

.avif)

.avif)

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

Understanding property investment returns is about more than just gross yields. Leveraged buy-to-let strategies can turn a modest 2% net yield into 7%+ ROCE, showing why calculating return on investment UK is essential for serious investors.

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

When you’re a busy professional, time is precious, and so is your capital. That’s why choosing the right property investments comes down to one question: how hard is your money working?

Most investors focus on yield, because it’s quick and simple. But yield only tells part of the story. A property showing a modest 2% net yield might look underwhelming, until you calculate the return on capital employed (ROCE). Suddenly, that same property could be delivering 7%+ returns.

In this guide, we’ll explain what ROCE is, why it matters more than yield alone, and how you can use it to measure the real return on your property investments.

ROCE measures your actual profit as a percentage of the cash you invested, not the property’s total value.

ROCE Formula:

ROCE = (Annual Profit ÷ Cash Invested) × 100

Why ROCE Matters

Unlike yield, ROCE accounts for leverage in property investment.

Example: If you buy a £280,000 property with a £70,000 deposit, your calculation uses £70,000 (plus costs) - not £280,000.

This is why professional investors prioritise ROCE over yield when assessing performance.

Yield vs Return on Investment: The Key Difference:

ROCE measures your actual profit as a percentage of the cash you invested, not the property’s total value.

ROCE Formula:

ROCE = (Annual Profit ÷ Cash Invested) × 100

Why ROCE Matters

Unlike yield, ROCE accounts for leverage in property investment.

Example: If you buy a £280,000 property with a £70,000 deposit, your calculation uses £70,000 (plus costs) - not £280,000.

This is why professional investors prioritise ROCE over yield when assessing performance.

Yield vs Return on Investment: The Key Difference:

Metric

Yield (on property value)

ROCE (on cash invested)

That’s leverage in action.

Metric

Yield (on property value)

ROCE (on cash invested)

Metric

Yield (on property value)

ROCE (on cash invested)

That’s leverage in action.

ROCE measures your actual profit as a percentage of the cash you invested, not the property’s total value.

ROCE Formula:

ROCE = (Annual Profit ÷ Cash Invested) × 100

Why ROCE Matters

Unlike yield, ROCE accounts for leverage in property investment.

Example: If you buy a £280,000 property with a £70,000 deposit, your calculation uses £70,000 (plus costs) - not £280,000.

This is why professional investors prioritise ROCE over yield when assessing performance.

Yield vs Return on Investment: The Key Difference:

ROCE measures your actual profit as a percentage of the cash you invested, not the property’s total value.

ROCE Formula:

ROCE = (Annual Profit ÷ Cash Invested) × 100

Why ROCE Matters

Unlike yield, ROCE accounts for leverage in property investment.

Example: If you buy a £280,000 property with a £70,000 deposit, your calculation uses £70,000 (plus costs) - not £280,000.

This is why professional investors prioritise ROCE over yield when assessing performance.

Yield vs Return on Investment: The Key Difference:

ROCE measures your actual profit as a percentage of the cash you invested, not the property’s total value.

ROCE Formula:

ROCE = (Annual Profit ÷ Cash Invested) × 100

Why ROCE Matters

Unlike yield, ROCE accounts for leverage in property investment.

Example: If you buy a £280,000 property with a £70,000 deposit, your calculation uses £70,000 (plus costs) - not £280,000.

This is why professional investors prioritise ROCE over yield when assessing performance.

Yield vs Return on Investment: The Key Difference:

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

Metric/Year

Investor A: All Cash

Investor B: Leveraged

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

Metric/Year

Investor A: All Cash

Investor B: Leveraged

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

Metric/Year

Investor A: All Cash

Investor B: Leveraged

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

When it comes to property investing, how you use your money can be just as important as how much you earn in rent. To illustrate the impact of leverage, let’s compare two investors, each with £300,000 to invest.

One chooses a straightforward all-cash approach, while the other spreads the same capital across multiple properties using deposits. The results highlight how return on capital employed can significantly boost wealth over time.

Join our investor briefings and stay ahead with expert insights, market updates, and priority notifications.

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Metric

Scenario 1:

Barking (High Yield)

Scenario 2:

Romford (Moderate Yield)

Higher-priced areas typically deliver lower rental returns, but stronger capital growth can balance the equation. Commuter belt areas often provide the sweet spot of reliable rental income and steady long-term appreciation.

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Metric

Scenario 1:

Barking (High Yield)

Scenario 2:

Romford (Moderate Yield)

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Metric

Scenario 1:

Barking (High Yield)

Scenario 2:

Romford (Moderate Yield)

Scenario 3: Zone 4 London (Lower Yield, Higher Growth)

Higher-priced areas typically deliver lower rental returns, but stronger capital growth can balance the equation. Commuter belt areas often provide the sweet spot of reliable rental income and steady long-term appreciation.

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Not all buy to let investments are equal. Yields and returns can vary widely depending on location, price, and growth potential. Here’s how three different property scenarios stack up side by side:

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

Understanding when to prioritise rental yield and when to focus on return on capital employed (ROCE) is key to shaping a property portfolio that matches your goals.

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

Tax Impact on Returns

Return on investment looks very different once tax is applied:

Company Structure Benefits

Owning property via a limited company can improve returns:

Refinancing for Return Optimisation

When property values rise or interest rates fall, refinancing can dramatically improve ROCE:

Tax Impact on Returns

Return on investment looks very different once tax is applied:

Company Structure Benefits

Owning property via a limited company can improve returns:

Refinancing for Return Optimisation

When property values rise or interest rates fall, refinancing can dramatically improve ROCE:

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

Tax Impact on Returns

Return on investment looks very different once tax is applied:

Company Structure Benefits

Owning property via a limited company can improve returns:

Refinancing for Return Optimisation

When property values rise or interest rates fall, refinancing can dramatically improve ROCE:

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

Tax Impact on Returns

Return on investment looks very different once tax is applied:

Company Structure Benefits

Owning property via a limited company can improve returns:

Refinancing for Return Optimisation

When property values rise or interest rates fall, refinancing can dramatically improve ROCE:

When you start factoring in tax, company structures, refinancing, and common pitfalls, calculating true property investment returns becomes more nuanced. This section highlights the key considerations that can significantly impact your return on capital employed, helping you make smarter, more informed investment decisions.

Tax Impact on Returns

Return on investment looks very different once tax is applied:

Company Structure Benefits

Owning property via a limited company can improve returns:

Refinancing for Return Optimisation

When property values rise or interest rates fall, refinancing can dramatically improve ROCE:

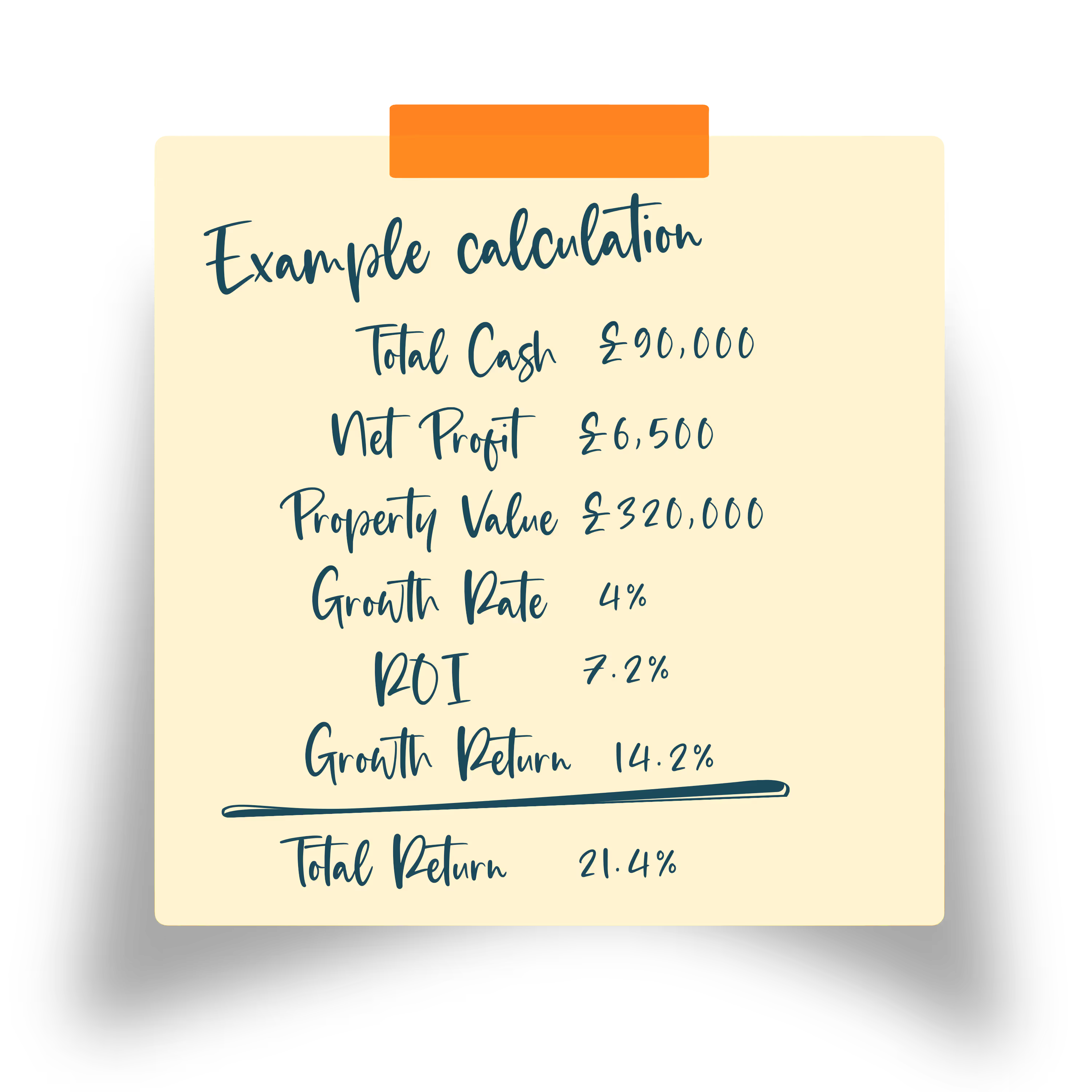

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Determine

total cash needed

Calculate

net annual profit

Apply

return formula

Add growth

component

Total return on

your investment

Ready to see what your investment could deliver? Follow these simple steps using our Investment Property Calculator:

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Our guide, Maximising Property Investment Returns, shows you exactly how professionals build stronger returns, from finance and tax planning to growth strategies.

Our guide, Maximising Property Investment Returns, shows you exactly how professionals build stronger returns, from finance and tax planning to growth strategies.

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Our guide, Maximising Property Investment Returns, shows you exactly how professionals build stronger returns, from finance and tax planning to growth strategies.

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Our guide, Maximising Property Investment Returns, shows you exactly how professionals build stronger returns, from finance and tax planning to growth strategies.

Understanding ROCE is just the beginning. Professional investors consistently achieve 15 to 20%+ total returns by combining ROCE optimisation with tax planning, portfolio diversification, value-add strategies, and smart market timing.

Our guide, Maximising Property Investment Returns, shows you exactly how professionals build stronger returns, from finance and tax planning to growth strategies.

See how past property investments delivered strong returns, from rental income to capital growth, these real examples showcase strategies that work.

Continue your property investment journey with these expert guides - practical strategies and insights to help you make smarter investment decisions.

Learn which mortgage structures give the best returns on UK property investments

Learn which mortgage structures give the best returns on UK property investments

Find out how to structure your portfolio for maximum tax efficiency and higher returns.K property investments

Whether you’re just getting started or ready to take the next step, we’re here for a no pressure, no obligation call, with just honest insight.

Choose a 15 minute intro chat or a full 45 minute consultation.